An insurance agency is a company that sells insurance products. Sometimes, insurance agencies are referred to as insurance brokerages. There are several types of insurance agencies. The two most common types of agencies are Captive Agencies and Independent Retail Agencies.

Captive agencies are companies offering insurance products through only one insurance carrier. Some common examples of captive insurance agencies are AllState, State Farm, and Progressive.

Whereas independent retail agencies have relationships with many different insurance carriers. These agencies shop among different carriers to find the best policy for their clients. They do not have a contract with any one insurance carrier.

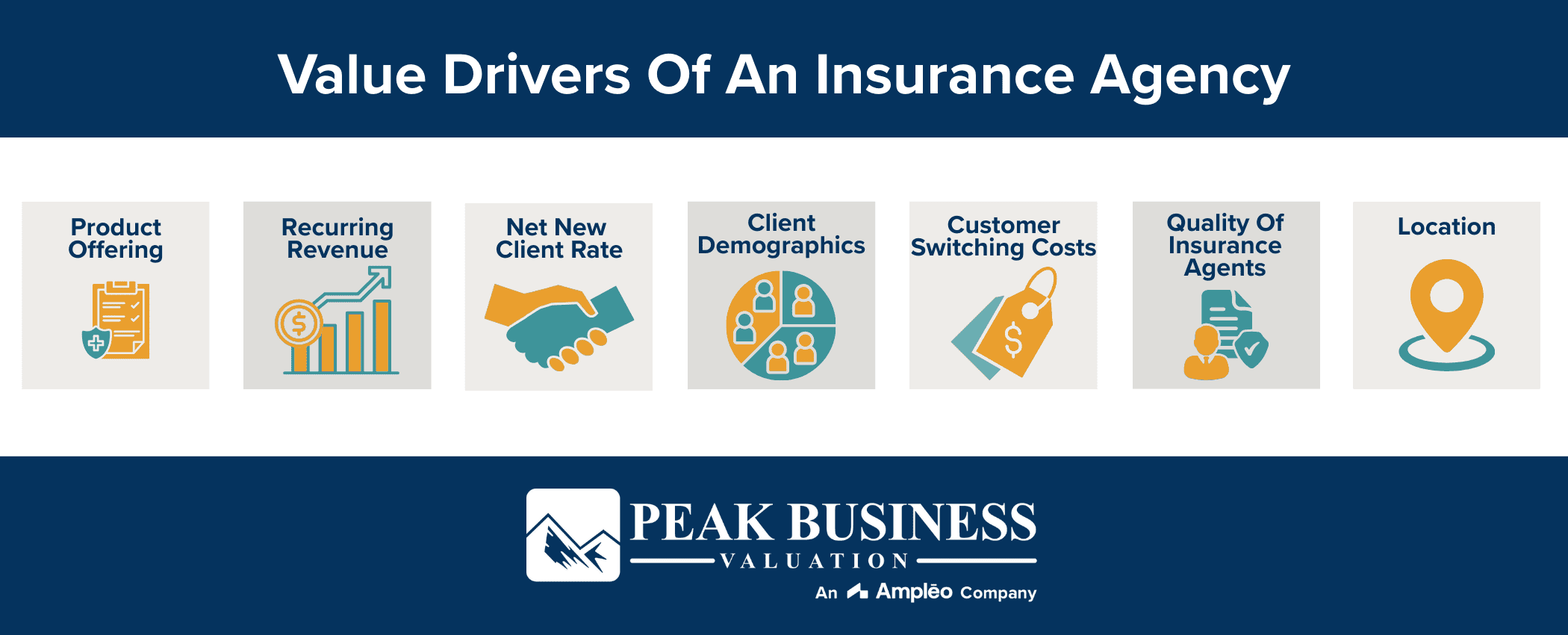

The following discusses several factors that impact the value of your Insurance Agency. These are value drivers of an insurance agency. A business valuation expert, like Peak Business Valuation, can help you better understand the value of your insurance agency. Schedule a free consultation to get started!

Insurance Product Offering

First, the strongest value driver of an insurance agency is the insurance product offering. Insurance agencies offer a whole host of insurance products. These products can include:

- Life insurance

- Homeowner’s insurance

- Auto insurance

- Health insurance

- Property and casualty insurance

- Liability insurance

- Other insurance products

What products does your agency sell? Insurance agencies make money from the commissions on the products they sell. The more products an agency is licensed to sell, the more likely the company is to produce higher revenues. Additionally, if you offer retirement products through an RIA, it can help draw clients to your agency.

Percentage of Recurring Revenue

Next, a valuation expert will consider what percentage of revenue is “recurring revenue“. One of the key value drivers for a successful insurance agency is recurring revenue. Most insurance products have a “renewal factor.” This renewal factor occurs when clients renew their insurance policies. If the client and the policy are already established, making the renewal process easy. The agent does not have to go out and find a new client or make a new sale. If a company has a high percentage of recurring revenue, the company is more valuable. Discover more on recurring revenue, by reading Growing Your Business Through Recurring Revenue.

Net New Client Rate

Is the company finding new clients faster than it is losing clients? If not, the new client rate is negative. This may be a sign that the company’s client base is unhappy with the current insurance agents. This may also mean the business and its revenue is declining.

Whereas, a positive net new client rate means the firm is attracting clients faster than it loses them. This is a good sign of growth.

Client Demographics

How old is your client base? Wealthy clients have more assets and need extra insurance products for coverage and protection. As such, a client base consisting of older, more mature clients will generally mean higher commissions and higher revenue. These clients are sometimes referred to as the “golden goose” clients.

On the contrary, younger individuals with fewer assets will require less coverage and protection. So, a book of business with many younger clients is not all bad. Younger clients might stay with you for a long time, which can result in larger commissions down the road.

Customer Switching Costs

Next, if the switching process is easy for your clients, there is an increased risk associated with your business. So, having high switching costs can encourage clients to stay with you.

Quality of Insurance Agents

Another value driver of an insurance agency is the quality of staff members or human capital. Good staff members are hard to find but they help keep customers happy. Low employee turnover will help create consistency with your clients and increase trust. Experienced employees will also help your company’s client retention.

Location

Last, where is your insurance agency located? Are you located in a highly-populated area or a small rural town? Is the income level of those in your location high, average, or low? Both of these factors can play a role in the value of an insurance agency. If you are in a highly-populated area, there will be more opportunities for increased clients. Similarly, if the majority of the population has a high income, there are likely more assets and more demand for insurance coverage.

Summary

As you can see, there are many value drivers of an insurance agency. Business valuation can be complex, so having a business valuation expert will help you better understand the value of your business.

Peak Business Valuation, business appraiser Utah, would love to speak with you about the value of your insurance agency. We can help you understand the value drivers that impact your business! Schedule a free consultation call with Peak today! To learn more, see the following articles:

- Valuing an Insurance Agency

- Value Drivers for an Insurance Brokerage

- Valuing Insurance Brokers

- How to Value an Insurance Agency

- Valuation Multiples for an Insurance Agency